3 Common Money Madness Traps to Avoid

Money makes the world go ’round, but some financial decisions can make our heads spin. Let’s dive into three common money madness blunders—backed by real life stories and some biblical wisdom. Why 3? Trust me, when it comes to our finances, there are a lot of pitfalls we could talk about… in my 20+ years as a financial advisor, I’ve seen most of them. But here are 3 that can be most devastating, that I want to warn you about. Don’t fall into these Money Madness Traps that can make you lose your financial sanity!

First, Don’t Live Paycheck to Paycheck

Let’s talk about Jake, a 32-year-old software developer, who makes six figures but always finds himself broke at the end of the month. He’s tried budgeting before, but he keeps losing track of his spending and overdrawing his checking account. Recently, when his car broke down, he had to put the $1,200 repair bill on his credit card, because he had no emergency fund!

Reality Check: Jake’s not alone… According to a recent article on marketwatch.com, a staggering 57% of today’s Americans (over half!) live paycheck to paycheck. (MarketWatch)

What does the Bible say about Jake’s situation?

“The wise store up choice food and olive oil, but fools gulp theirs down.” – Proverbs 21:20

Saving for the future is a wise thing to do, according to the Bible. Conversely, spending all you have is foolish, according to Scripture. And yet, that’s how the majority of Americans live … paycheck to paycheck, not saving anything for the proverbial “rainy day”.

What happened to Jake? Thankfully, he finally created a budget and found some ways to dramatically cut his spending each month. Then, he set up an emergency fund account to automatically draft this same amount of new found cash from his checking account each month, so that his new emergency fund would be fully funded within 12 months. Finally, he paid off his credit card, cancelled it, and destroyed all the evidence. Great job Jake!

A foundational “method to my money” is learning the importance of storing up for the future, instead of consuming everything we have today. This is counter cultural. How many times have we heard phrases like, “be present” and “live for the moment”. Certainly, there is truth in the fact that we won’t be here on this earth forever. Yes, we should enjoy every day we have been given to the fullest, because we aren’t promised tomorrow! But enjoying every day to the fullest is not the same as spending every dollar to the fullest! And, surprisingly, a strange enjoyment can be found in setting aside a portion of our income to protect ourselves and those we love.

Second, Don’t Wait to Invest!

Lisa, a 25-year-old marketing professional, thought retirement was something “future Lisa” would worry about. Instead of investing in her 401K, she spent her extra cash on vacations, clothes and concerts. A decade later, she met with a financial planner and realized she should’ve started investing sooner.

Reality Check: Thanks to inflation (“the silent thief” as I like to call it), the old way of simply saving money at a bank or credit union just won’t cut it anymore. If inflation is devaluing your dollar by 3% each year, and your bank is paying you 2% on your savings, you’re losing money! That means you’re paying the bank to hold your money for you, how is that fair? But thanks to compounding interest (or as some call it, the “snowball” effect), even small investments made early in life can grow into a huge nest egg over time. As a matter of fact, investing early is even more important than how much you actually invest! Consider the following from “11 Charts Showing Why You Should Invest Today” by U.S. News and World Report:

Investing Early Is a Key to Long-term Success

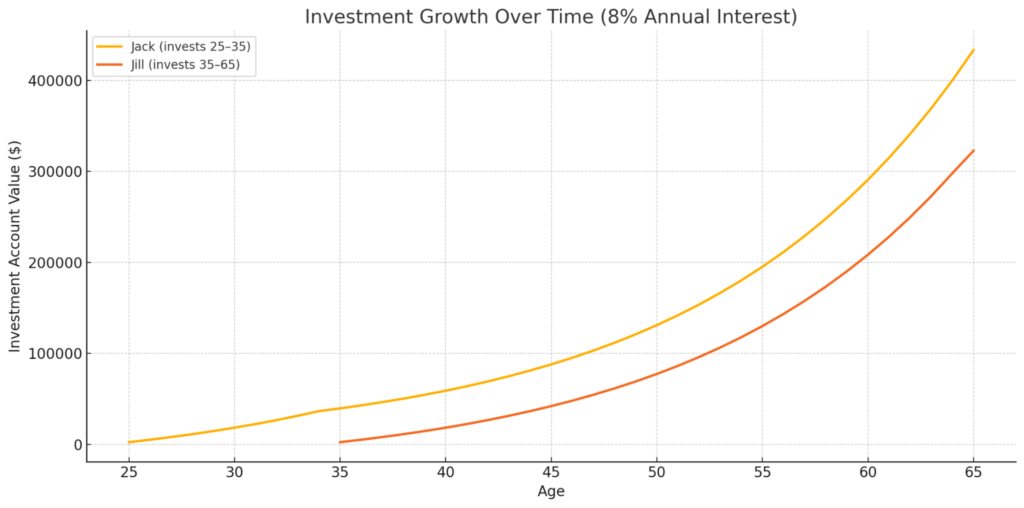

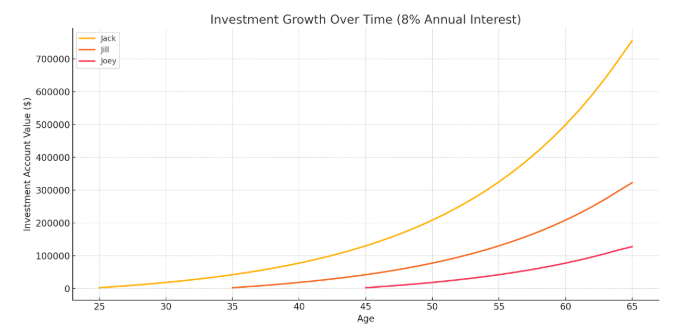

“The stock market is kindest to those who stay faithful to it longest. To see this in action, consider investors Jack, Jill and Joey.

Jack starts investing $200 per month when he’s 25. By age 65, his portfolio is worth more than $700,000.

Jill doesn’t start investing until age 35. She also contributes $200 per month, but by 65, her portfolio is only worth about $300,000. By waiting 10 years to start, she ends up with less than half of what Jack accumulates.

Joey, the late bloomer, starts investing $200 per month when he’s 45, and after 20 years he has just a little more than $100,000.

Jack invested $200 per month starting at age 25, contributing $96,000 total over 40 years. Jill invested $200 per month starting at age 35, contributing $72,000 total over 30 years. Joey invested $200 per month starting at age 45, contributing $48,000 total over 20 years.” All three in this example, earned the same 8% per year compounding return, but the results are substantially different!

Now so far, what I’ve shared makes sense. Jack invested more, over a longer time period… it makes sense that he would have more in retirement.

But Time invested is so important that Jack can even stop adding to his investments [after just 10 years] and still have more than Jill at age 65.

If Jack were to contribute $200 per month from age 25 to 35 – contributing only $24,000 over 10 years – his investments would be worth over $400,000 at age 65.

But if Jill continually invests $200 per month between ages 35 and 65, she only ends up with a little over $300,000 at 65. Even though she contributed three times as much as Jack over her lifetime ($72,000), because she missed those first 10 years of investing, Jack would have more.

What happened to Lisa? At 35, she met with a financial planner and they calculated how much she needed to invest monthly to ultimately reach her retirement spending goals. Then, they figured how much she needed to set aside for emergencies. Next, she set up an investment account and an emergency fund to automatically draft her checking account each month for these amounts, within 5 days after her paycheck is deposited. The first few months were tough, but she quickly adjusted to her new spending level and began to feel more confident, as she watched her accounts grow.

Scripture says, “Go to the ant, you sluggard; consider its ways and be wise! It has no commander, no overseer or ruler, yet it stores its provisions in summer and gathers its food at harvest.” – Proverbs 6:6-8

This verse teaches us the power of preparation for a season ahead — investing now, while we are able to work, so that we have what we need in the years ahead when we might not be able to do so, is like the ant storing food for the winter.

Over the years, I’ve met with many couples to discuss investing for retirement. It’s amazing to me the different attitudes I encounter. Some consider retirement to be so far away… to them, it just isn’t very important. Their perspective is that preparing for retirement shouldn’t interfere with their lifestyles in the here and now.

To my friends in this group, I would remind you that there is biblical wisdom in setting aside a significant portion of your income now to prepare for the final 30+ years of your life. Save 10-20% of your income, and live on what’s left. Your future self will thank you!

I’ve met with others who are on the opposite side of the retirement planning spectrum. They seem so concerned about their retirement years that they are paralyzed with fear. Will we have enough? What if the stock market crashes and we lose everything we’ve worked for? What if we get sick and healthcare costs are too high? Will we be ok?

If this describes you, I will admit I’ve been right there with you… and at times I still struggle with thoughts like these. Please join me in remembering the words of our Lord, “Who of you by worrying can add a single hour to your life? Since you cannot do this very little thing, why do you worry about the rest? Consider how the wild flowers grow. They do not labor or spin. Yet I tell you, not even Solomon in all his splendor was dressed like one of these. If that is how God clothes the grass of the field, which is here today, and tomorrow is thrown into the fire, how much more will he clothe you—you of little faith! And do not set your heart on what you will eat or drink; do not worry about it… But seek his kingdom, and these things will be given to you as well.” (Luke 12:25-29,31)

So, in balance, we see that there is biblical wisdom in setting aside a portion of our income now, and investing it for a future season when our income is uncertain. And yet, we are also instructed by our Lord not to worry about our future. We can have faith that our loving heavenly Father will provide what we need, both now and in retirement, when we seek His kingdom.

That brings us to our third and final Money Madness Trap: Ignoring the Needs of Others

Ok, this is where I’m going to sound a little preachy, and I don’t mean to be. But I’ve learned over the years that when I’ve stepped out on faith to help someone, my needs have always been taken care of. There’s a biblical principle here that is meant to set us free, and bring us a ton of joy. And yet, oftentimes our fear of what might happen to us if we give, can cause us to miss out.

In Luke 18:18-24, we read a story that can help us here, I think. “A certain ruler asked him, “Good teacher, what must I do to inherit eternal life?” “Why do you call me good?” Jesus answered. “No one is good—except God alone. You know the commandments: ‘You shall not commit adultery, you shall not murder, you shall not steal, you shall not give false testimony, honor your father and mother.’” “All these I have kept since I was a boy,” he said. Jesus said to the rich young man, “One thing you still lack. Sell all that you have and distribute to the poor, and you will have treasure in heaven; and come, follow me.” When he heard this, he became very sad, because he was very wealthy. Jesus looked at him and said, “How hard it is for the rich to enter the kingdom of God!” Why did Jesus say that? Does He require that we sell everything and give it all to the poor before we can be his disciple? Well, no. We see plenty of other places in Scripture where people were not asked to give everything away, so that can’t be right. But we see a principle here that is helpful… this young man was asking how he could receive eternal life (in other words, go to heaven and live forever). Jesus told him to keep the commandments, but the man responded that he had kept the commandments since he was a boy. He is very religious. Truth is, he hadn’t… no one has kept all of the commandments perfectly except for Christ. But Jesus, knowing what was in this man’s heart, said for him to sell everything and give it all away. But that was the man’s issue… he couldn’t do that. He was rich and he loved his money too much to give it away.

I believe we are NOT told to be generous and help those in need because, if we don’t, they won’t be helped. No, God owns everything and he can give wealth to whomever he wants whenever he wants. The reason we are told to be generous is to test our own hearts. Which is more important to us? God or our money? Are we willing to trust God to give of our resources to help others, and trust Him to take care of our needs? Are we willing to trust him to make us happy? Or do we hoard what we have, ignoring the needs of others, so that we can try to make ourselves happy? Friends, God knows you and me better than we know ourselves. He knows all about us because he made us. He knows exactly what we need to be happy, and his plan is always good. Trust Him to give you what is best for you, and generously give to those in need. This will result in spiritual blessing far greater than a fat 401(k) or retirement home at the coast.

The Bottom Line

We’ve all made money mistakes, haven’t we? Plenty of them! And they can certainly lead to feelings of frustration and “madness”. But here’s the good news? At Method To My Money, we’re here to help you make a change. We’ve discussed 3 Common Money Madness Traps: Living Paycheck to Paycheck, Waiting Too Long to Invest, and Ignoring the Needs of Others. And we’ve shared some time-tested biblical methods to help us choose a better way… if you like what you’ve heard please reach out and let us know! And considering sharing this with a friend. And if you’re interested in talking with a financial coach, click the “Talk with a Money Coach” link to schedule a time. I’m Matt Hearn, and this is MethodtoMyMoney.com.